Indexed Annuities - Anatomy of a financial scam

Oct 20, 2017

A year ago, I got a look at a financial product being offered primarily to seniors. It came with the recommendation to put all of their retirement savings into it. The product was called an "equity-indexed annuity" (aka "fixed index annuity").

The marketing sounds great

The company selling this was Global Atlantic Financial Group, but there are lots of these. All of these products are losers for the investor, regardless of the company.

Here are some plans from their marketing brochure:

And their webpage on Fixed Index Annuities.

The sound bite is:

"Upside potential with downside market protection"

What they are suggesting is:

- Stock market goes up: your investment goes up approx the same amount.

- Stock market goes down: your investement is unaffected.

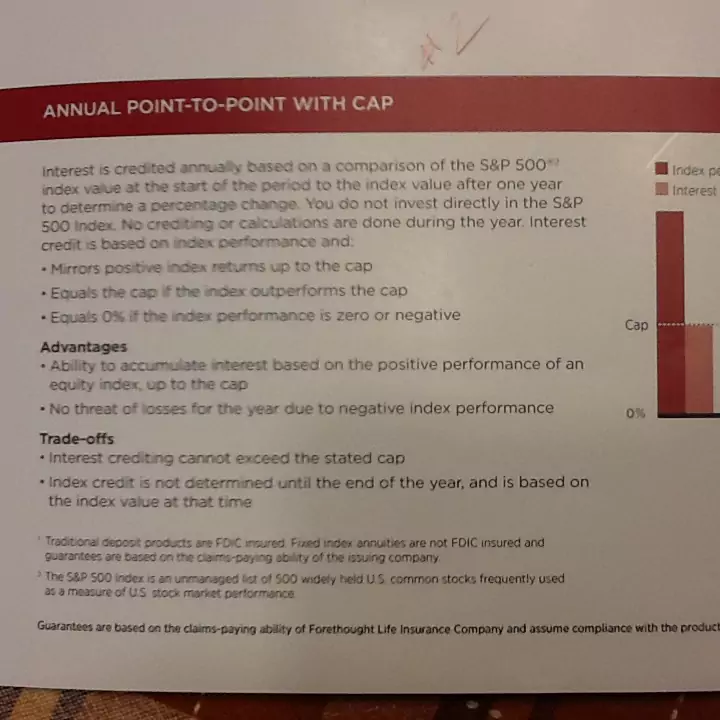

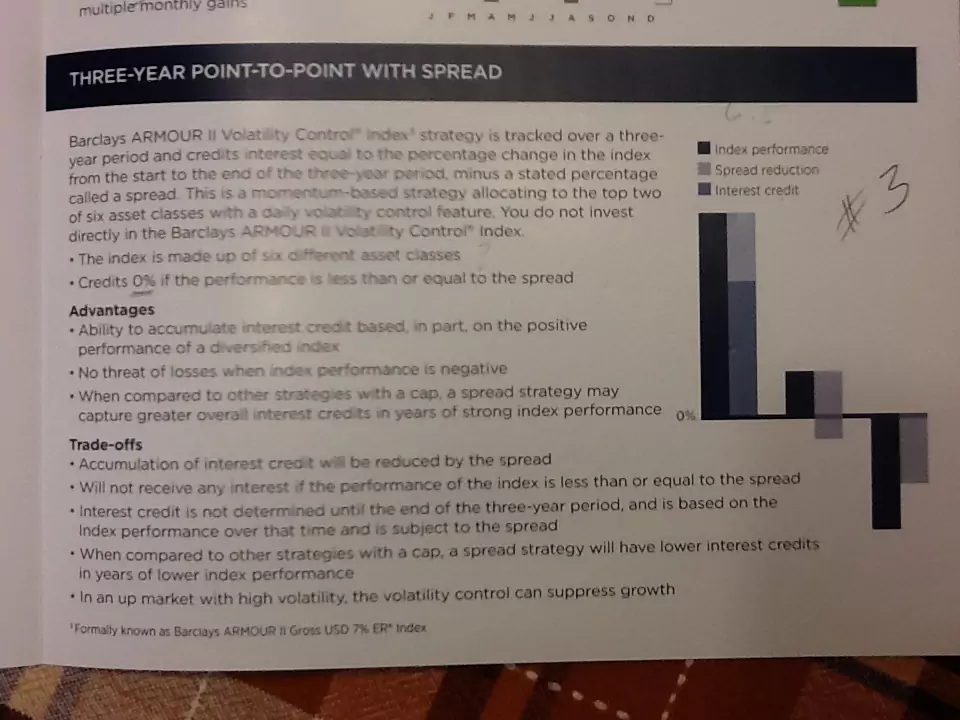

The marketing then explains how this isn't a free lunch and there is a minor tradeoff involved where you don't get the full market upside. Possible ways this is structured include:

- The market upside is capped at a certain amount per year

- The market upside is reduced by a certain percentage (a spread).

- If the growth is less than some amount, you get no upside.

- Some combination of these and other clever schemes.

I'm guessing this tradeoff is pointed out in marketing materials because their customers know that a free lunch means a scam. By showing one of the less significant downsides, it disables people's scam detectors.

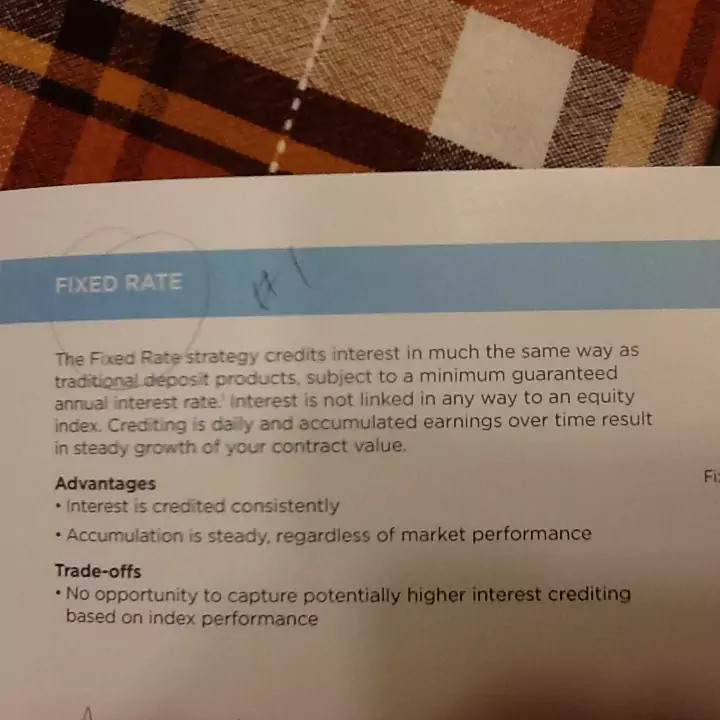

Lastly, there is even a fixed-rate plan that sounds like a savings account, but it's still an annuity. Take a look:

Short on details

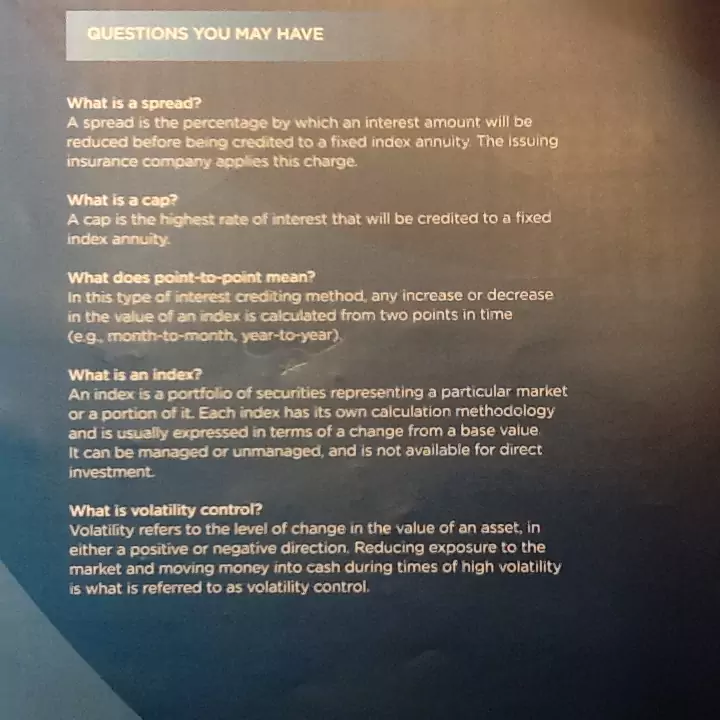

Neither the website nor the brochure has any real details. Perhaps that's because I simply haven't yet shown you the image of the brochure that explains everything:

If you don't know what an index is, you might not be in for a fair fight.

There is also a page of fine print that is essentially a liability waiver, but even with that, critical components of how this works are completely missing:

- What number is the cap percentage?

- What number is the spread percentage?

- How is the market growth calculated?

- What is the guaranteed minimum interest rate?

- What is the initial fixed interest rate?

- How is interest compounded?

- How often can the interest, cap, and spread numbers be modified?

- What fees are charged?

- What are the early-surrender penalties?

- What happens if I die?

Don't look behind the curtain

There are lots of knobs here that affect the performance of these products. The more knobs, the more ways exist for the customer to be fleeced. Lets look at some of the tricks of the trade.

"Fixed" Interest Rate

This plan sounds much like a savings account at a bank, and should feel familiar. The salesperson will probably ask what interest rate your bank gets: "Oh, it's only 0.34%" and will then explain that this interest rate is currently 0.4% or something along those lines. Sounds great.

Unfortunately, that could be a teaser rate. Maybe the actual rate drops much lower after a few months. Who knows? When I looked into the "minimum guaranteed rate" on this fund, the minimum was actually 0.0%. It's unclear what this "minimum guaranteed rate" actually guarantees.

There are also outright lies. In the brochure, it is mentioned that both "interest is credited consistently" and "crediting is daily", meaningless phrases. What you are supposed to confuse this with is "interest is compounded continuously" or "compounding is daily", which have a specific meaning that is regulated.

The frequency of compounding affects how much money you get. Compounding more frequently gives you more money. Consider $1,000 invested at a 5% interest rate for 1 year, with different compounding rates:

| Compounding frequency | Interest after 1 year (aka APY) |

| Annual | $50 |

| Monthly | $50.63 |

| Daily | $51.27 |

You think you are getting daily compounding, or better, but you are getting the annual rate. A bank savings account is regulated so that they must tell you the effective APY (Annual Percentage Yield) which is the rate over 1 year, regardless of which compounding method is used. An annuity has no such regulation imposed on them, so they use terms like "crediting is daily". This makes comparing to your bank's interest rate an apples-to-oranges comparison.

FDIC Insurance

Remember that little thing called FDIC Insurance? This is where, if a bank goes bankrupt, your savings account is safe and insured by the federal government. Annuities are not FDIC insured. If the annuity company loses money, you might not get yours back.

I'm far from an expert in evaluating company's financial health. Global Atlantic, the company mentioned above, used to be a devision of Goldman Sachs until 2013. This is the same Goldman Sachs that received a $10B bailout during the financial crisis and admitted last year to the Justice Department that it knowingly defrauded investors in 2008. Goldman Sachs sold Global Atlantic im 2013 because regulators required the company to have lower financial risk, so it spun off a separate company and based that company in Bermuda.

Spreads and Caps

Let's start with the dividend lie of omission. Market returns are measured in both the increase in value of the stock and dividends. Dividends, which are always positive, get left out from all of these fund calculations. Any dividends recieved from investing your money are kept by Global Atlantic. You would be getting those in a Mutual Fund. The S&P index historically has an median annual 11% return and 3% dividends. Even ignoring spreads and caps, you are missing out on dividends, which go straight to the fund owner's pocket.

The spread or cap number makes a ton of the difference. Why is this number not in the brochure? It's literally the most critical bit of information. That's insane.

Here is a pdf I found showing the actual spread, cap, and interest rates for some of these funds, at the start of 2017. The PDF states "Not for use with the public" as the rates you are agreeing to are apparently a secret. I don't know for certain that these rates are accurate, but I have no reason to suspect otherwise.

For the 'Capped' plan, They cap your earnings at 4.25% per year. For a 'Spread' plan, they keep the first 3.5% of your earnings per year before you see a penny.

If you are confused, and aren't able to tell if that's a lot or a little, that's the whole point. I'll try to explain with some historical data.

If you look at the S&P median annual returns, you see that a typical year has 14.31% returns. In such a year, $1,000 invested would look like:

- S&P mutual fund would grow by $143.10

- 4.25% capped fund would grow by $42.50

- 3.5% spread fund would grow by $108.10

This is a hypothetical example, but we can simulate these 3 funds fund types in all years of the S&P with a small spreadsheet.

Columns E and H show the returns that the Annuity would have had above and beyond the S&P if invested on Jan 1 of that year and kept for 1 and 3 years respectively. Green cells are years where the annuity had better returns, red cells where the S&P did btter, and the number in the cell shows by how much one did better than the other. Not a lot of green.

Over 1 year periods the S&P averaged 11.74% return, and the 1-year Capped annuity averaged 2.86% return. If you invested $1,000 in both for 6 such years, you would have made about $760 more with the S&P than the annuity.

Over 3 year periods, the S&P averaged 38.93% returns while the 3-year spread annuity averaged 22.31% return. If you invested $1,000 in both for 6 such years, you would have made about $440 more with the S&P than the annuity.

You can see how the dividend theft, combined with high fees in the form of caps and spreads, mean most of the market return goes to the annuity company and not you the investor.

You might agree but still argue that you may need access to my money in a short term, and in that case the "no downside risk" is worth the very high cost of some of the upside. You would almost certainly still be wrong because of early surrender.

Early Surrender

Not mentioned anywhere in the brochure, there is a clause in your annuity contract that states that there are penalties for taking money out of your annuity early. How early is too early? The answer is typically any time within 10 years of purchasing the annuity.

Don't believe me? Take a look at this Multiple Annuity Rates PDF. The Global Atlantic rates are on page 7, but you can look at a bunch of companies here. See the section labelled "Surrender Charges" with the text below that reads "(10 Year) 10 - 10 - 9 - 9 - 8 - 7 - 6 - 5 - 4 - 2 - 0". What this text tells you is the fee that will be charged if you choose to cash out your annuity in each of the years after opening it. In the first 2 year's it's 10%, in the next 2 years it's 9%, etc:

| Years after Opening | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11+ |

| Fee | 10% | 10% | 9% | 9% | 8% | 7% | 6% | 5% | 4% | 2% | 0% |

This means that if you buy this annuity and expect to be able to take money out when you need it, in the short term, you will be losing as much as 10% of your investment right off the top. Not 10% of the earnings, but 10% of your entire investment. $100 of every $1,000. Years of your life savings.

Many of the funds have even worse surrender fees than this one, even as high as 20%!

So, because of the ongoing fees (spreads and caps) you lose more and more money the longer you've invested. And because of the early surrender fees, you lose more money the shorter you've invested. Fleeced either way.

Commissions

The moment you sign over your retirement savings to an annuity provider, without telling you, they immediately take about 10% of your hard-earned money for themselves. Then, every year, they also take over half of the growth you should have earned in the market. They never tell you this, you don't get billed, it's just that your earnings are that much lower and you pay when you want the money back in early surrender.

If you aren't convinced, take a look at this Schedule of Commissions PDF, on page 2. This shows the commisions paid to the "financial advisor" who sold you this annuity. Depending on your age and which "Fixed-Indexed Annuity Product" you were sold, they will get as much as 8% of your money as a commission "at issue", and another 1% or so of your money every year ("annual trail") that your money stays invested in the fund. That's just the salesperson's commission, not what the actual company is making in profit.

It gets uglier. See this Bonus Commission PDF for the salespeople, which reads "The more you brew, the more you accure. ... Enjoy the bold flavor of 7% commissions plus an additional sweetener - incentive compensation based on annual production." with pictures showing up to an extra 2% commission for selling over $3 million dollars in annuities in a year. I hope that "additional sweetener" helps them swallow the guilt from the theft of other's retirement savings.

For many people, this commission represents literal years of their life of saving money.

Don't take my word for it

- Forbes: The Truth about Equity-Indexed Annuities

- Financial Industry Regulatory Authority: Equity-Indexed Annuities - A Complex Choice

- Dateline MSNBC: Tricks of the Trade

- CBS News: Congress Sells Out Seniors: No SEC Regulation for Indexed Annuities

Regulations: What is a "Financial Advisor"?

Many of these salespeople will introduce themselves as a financial advisor. This sounds like they are on your side. It sounds official, like "certified electrician", and you might expect they have certifications and are regulated. They might, but they don't have to be. The term Financial Advisor has no legal meaning.

Worse, annuities aren't regulated like investment funds. Normally, something like this wouls be regulated by the Securities and Exchange Commission (SEC). However, despite the fact that they are marketed just like Mutual Funds, they are considered "insurance products" and are thus not under the Jurisdiction of the SEC. For the most part, individual states must regulate these, and few are equipped to do a very good job.

This industry makes $17 Billion profit per year from families retirement savings, and lobbies hard to remain unregulated to keep this money flowing.

In 2016, the Department of Labor, under Obama, put forth a new rule that would require a financial services company to disclose their commissions and have a "fiduciary responsibilty" to their clients. A fiduciary responsibility means that by law, they must recommend investments that are best for their client's financial interest (rather than best for commissions). If they fail to do so, they can then be taken to court. In addition, annuity vendors will have to disclose their commissions to clients.

The financial industry fought back hard, including awful ads like these:

Plot twist: Anne is actually stealing the college fund.

Obama's Department of Labor caved a little and delayed implementation of the rule to June 2017.

A very early priority of President Trump, Trump signed a memorandum less than 2 weeks after taking office that instructed the Department of Labor to delay the rule by an additional 6 months. A few days later, he appointed Department of Labor Secretary Alexander Acosta to make sure this got implemented.

The Department of Labor in March began a 15-day public comment period on these delays, during which they recieved about 193,000 comment letters, with nearly 178,000 opposing the delay. After the comment period, they recommended a 2 year delay until June 2019, which was approved by the White House in August 2017.

It is reasonable to imagine that the current administration will continue to delay or weaken this rule rather than allow it to take place in 2019.

Blog of Greg Grothaus.

Software Engineer at Google. Outdoor adventurer type. Opinions expressed here are mine alone.